In 2022, the global photovoltaic market will develop rapidly, and the scale of China, Europe, Latin America and other markets will increase significantly, attracting many companies to cross-border entry into photovoltaics, with the most involved being the cells and components. Sobi Consulting predicts that the world's newly installed photovoltaic power generation capacity (DC) will exceed 260GW in 2022, of which more than 90% of the components will come from Chinese companies. It is no exaggeration to say that China’s photovoltaic industry has made a huge contribution to global carbon peaking and carbon neutrality.

After intense research visits and data verification, Sobi Photovoltaic Network & Sobi Consulting jointly launched the 2022 Chinese photovoltaic module company shipment list. From what we know, the global photovoltaic market will be even hotter in 2022, with leading companies frequently expanding production and market concentration further increasing. According to statistics, among the companies participating in this information statistics, the top 10 shipments totaled more than 240GW, a year-on-year increase of about 60%, and their share of global photovoltaic module demand increased to more than 90% (more than 75% in 2021).

Illustrate:

1. All data are summarized by Sobi Photovoltaic Network & Sobi Consulting through telephone surveys, supplier visits, customer visits and other channels, combined with bidding information, supply contracts, etc. Please indicate the source when reprinting.

2. The statistical caliber is brand shipments, including self-use, but does not include products manufactured for others.

3. This data is not used as a basis for investment or procurement. If it is inconsistent with the company's actual shipments, the announcement by the listed company shall prevail.

In 2022, the threshold for China's top 10 photovoltaic module companies will reach 7GW, more than doubling, which is also in line with the industry's previous expectations. Sales leaders of many component companies said that only the first quarter of 2022 can barely be considered an off-season. After that, the market has been very hot. Most companies' shipments in the first three quarters have exceeded that of the whole of 2021, and supply and demand are both booming. Especially in Europe, even if it cannot be installed immediately, components must be purchased to stock up.

At the same time, many companies have proposed large-scale production expansion plans, and shipment targets for 2023 have also been significantly increased. Sobi Photovoltaic Network & Sobi Consulting learned that the shipment target of the Top 10 module companies in 2023 alone will reach about 400GW, which has exceeded the global module demand in 2023. This means that the market competition will be more intense this year, and the concentration is expected to remain Rising trend. According to assessments, there may be around eight companies with module shipments exceeding 25GW in 2023.

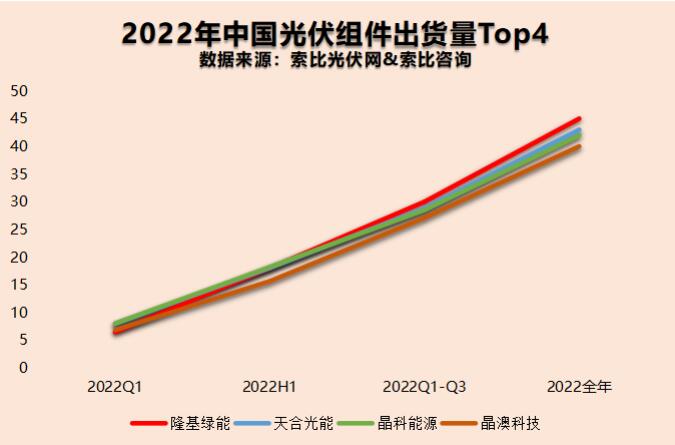

Specifically, LONGi, Trina, Jinko, and JA Solar continue to rank among the top four. In 2022, global shipments will total about 170GW, accounting for about 2/3 of the world's newly installed capacity, widening the gap with other companies. In this regard, we believe that the leading role of leading companies in technology and market is very obvious. Whether it is overseas channels or domestic bidding, they are the first choice of many development and investment companies, and have been widely recognized by owners and financial institutions. It is expected that the module shipments of these four companies will exceed 240GW in 2023.

The popularity of overseas markets has attracted the attention of many photovoltaic companies. According to statistics from the China Photovoltaic Industry Association, 144 countries around the world have set quantitative targets for renewable energy development, and the total exports of photovoltaic products from January to November 2022 reached US$47.75 billion. From what the author has learned, in addition to the above four companies, companies such as Canadian Solar and Risen Energy also have an overseas share of more than 60%. Zhengxin Optoelectronics and Anhui Daheng have an overseas share of 80% and 80%, respectively. 90%.

2022 is called the first year of the development of n-type battery components. According to statistics from Sobi Photovoltaic Network & Sobi Consulting, the shipment volume of TOPCon and HJT modules has exceeded 20GW, among which JinkoSolar’s n-type TOPCon module shipments exceeded 10GW. Considering the impact of n-type components on p-type components The price difference has narrowed to less than 5 cents/W (refer to China Power Construction's 26GW module procurement tender), which is more economical in many photovoltaic projects. In 2023, n-type module shipments may reach 60-70GW.

Judging from the actions of major photovoltaic companies, except for LONGi Green Energy, which is developing HPBC, the new production capacity of other companies is basically n-type. Trina Solar said that n-type production capacity will reach 30GW in 2023, and shipments will exceed 20GW; JinkoSolar revealed that n-type products will account for more than 50% of production capacity and shipments in 2023; Oriental Sun Sheng proposed that the production capacity of n-type HJT battery modules will reach 15GW in 2023; a new energy introduction said that the production capacity of n-type cells and modules will each be 30GW in 2023, fully embracing the n-type era.

Source: Sobi Photovoltaic Network

E-mail: info@chemborun.com

E-mail: info@chemborun.com Tel: +86-574-87178138

Tel: +86-574-87178138  No. 1558, Jiangnan Road,, Ningbo, Zhejiang, China (Mainland)/31

No. 1558, Jiangnan Road,, Ningbo, Zhejiang, China (Mainland)/31